Filter

Contents

Front Ratio Spread: Everything You Need To Know

Contents

What is a Ratio Spread?

A ratio spread is a high-probability trading strategy with a big profit window due to the embedded long spread. The setup of this undefined-risk trade is a combination of both long and short options of the same type (call or put). The most common ratio will be ‘2:1’, selling twice as many short options against the long options, and ultimately “financing” the cost of the long spread with an extra short option and turning the trade into a net credit.

As a trader, you’ll use front ratio spreads to act on a directional bias:

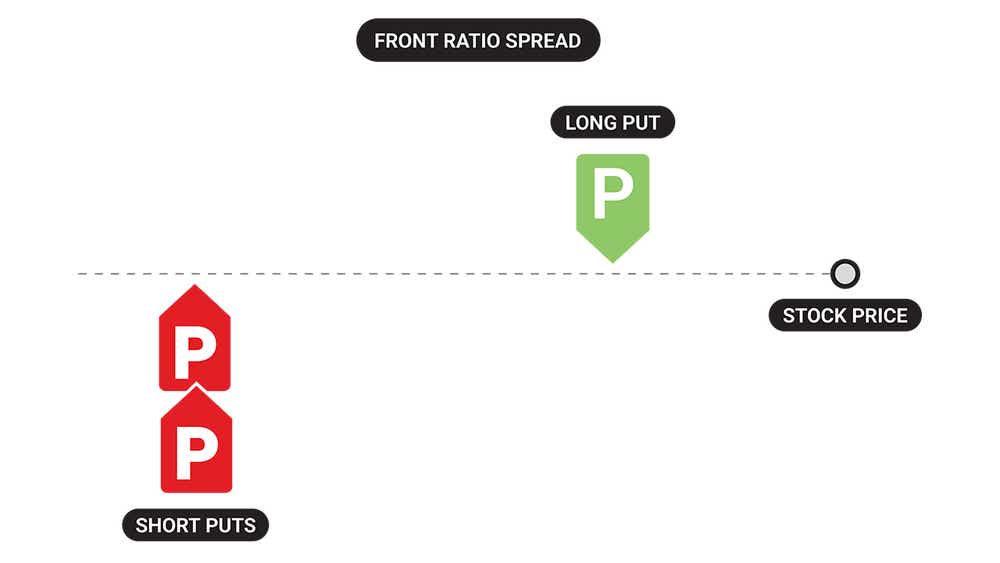

- A front ratio spread is created by purchasing a put or call debit spread with a higher quantity of short puts or calls at the short strike of the debit spread to chance the net debit price to a net credit

- The ideal implied volatility (IV) is high

- A call ratio spread consists of a long call and a larger quantity of further OTM short calls

- A put ratio spread is the combination of a long put and a higher quantity of further OTM short puts

- The put front ratio spread has a long delta bias which will profit from the underlying moving higher and the strikes expiring OTM, or slightly lower to the strikes of the short options where max profit is realized

- The call front ratio spread has a short delta bias which will profit from the underlying moving lower and the strikes expiring OTM, or slightly higher to the strikes of the short options where max profit is realized

Strategy Overview

Definition

A ratio spread consists of an options spread where there are more contracts on one strike than another. A front-ratio spread has more short contracts than long contacts, where a back-ratio spread has more long contracts than short contracts.

Directional Assumption

Front ratio spreads are considered omni-directional trades when we route them for a credit, because we have no risk and a small profit to the OTM side, but our max profit is actually to the ITM side if our short strike is right on the stock price at expiration.

Put front-ratio spreads have a positive delta to start and no risk to the upside, but max profit is to the downside at the short strike.

Call front-ratio spreads have a negative delta to start and no risk to the downside, but max profit is to the upside at the short strike.

Ideal Implied Volatility Environment

High IV environments are ideal for ratio spreads because extrinsic value is higher with far OTM strikes. This means that we can make the embedded spread wider and still collect a credit, where in a low IV environment we will not be able to make the ratio spread very wide at all while still collecting a credit.

The wider our spreads are, the better our breakeven price will be, as the long embedded spread’s value offsets our risk past the short strike.

We can also collect more premium up front with narrow front ratio spreads in a high IV environment compared to the same-width front ratio spread in a low IV environment.

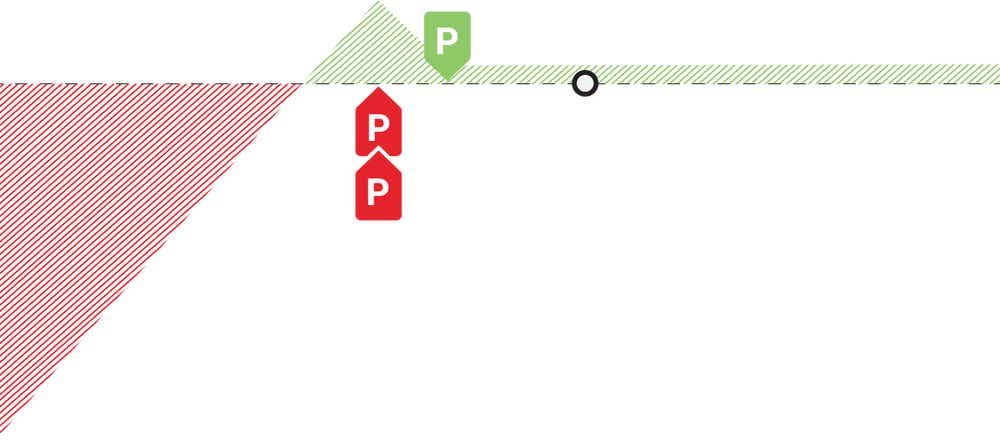

Put Front-Ratio Spread

A front ratio put spread is a neutral to bearish strategy that is created by purchasing a put debit spread with an additional short put at the short strike of the debit spread. The strategy is generally placed for a net credit so that there is no upside risk.

PROFIT/LOSS CHART

DIRECTIONAL ASSUMPTION

IDEAL IV ENVIRONMENT

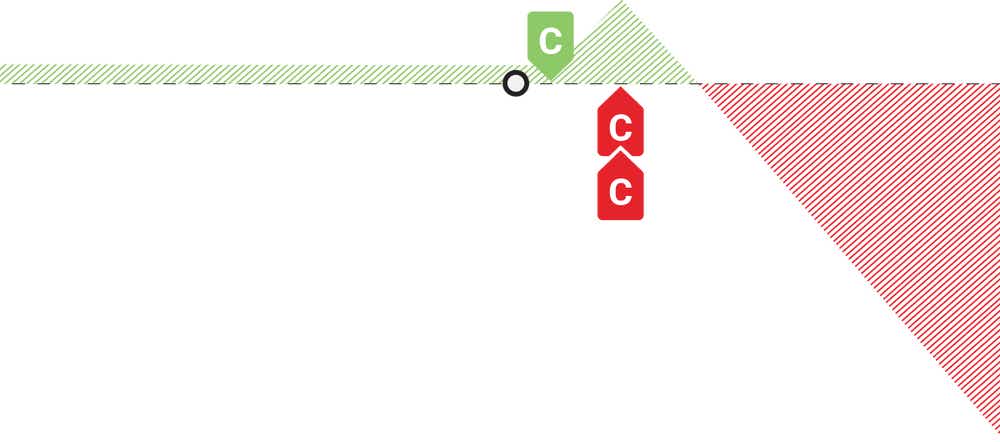

Call Front-Ratio Spread

A front ratio call spread is a neutral to bullish strategy that is created by purchasing a call debit spread with an additional short call at the short strike of the debit spread. The strategy is generally placed for a net credit so that there is no downside risk.

PROFIT/LOSS CHART

DIRECTIONAL ASSUMPTION

IDEAL IV ENVIRONMENT

Front Ratio Spread Strategy: How It Works

In other words, with put ratio spreads that are routed for a credit, you won’t have any risk if the underlying’s price moves higher; and with call ratio spreads routed for a credit on trade entry, you won’t have any risk if the underlying’s price goes down. Both of these strategies have no risk to the OTM side, but max profit is actually realized to the ITM side, so we like to think that if you have very little credit up front and you have a really wide embedded spread, you want the strikes to move ITM. But if you collect a large premium up front and have little additional profit potential on the ITM side, you probably want the strikes to remain OTM.

Setup of a Front Ratio Spread

This is the typical format of a front ratio spread:

Front Ratio Call Spread

| Front Ratio Put Spread

|

Front Ratio Spread Strategy Example

Suppose you’re neutral, but mildly bullish on Company XYZ because you believe the price will only rise slightly. You enter a front ratio spread with calls when the shares of the stock are trading at $107.00 – you buy a $110.00 call with 60 days to expiration (DTE) for $5.00, and sell two $115.00 strike calls for $3.00 each.

One options contract represents 100 shares. You pay a premium of $5.00, costing you $500.00 ($5.00 x 100) for the long position. When you sell the short calls you receive a premium of $3.00 per contract, which comes to $600.00 ($3.00 x 200 shares) in total extrinsic value premium. This gives you a net premium (credit) of $100.00 ($600.00 credit – $500.00 debit).

Fast-forward 60 days and you’re at expiration.

If the stock is trading at $115.00, you would have a $5.00 profit on the long spread’s value, and you collected $1.00 up front, leaving you with the max profit of $6.00 or $600.00 real dollars.

If the stock is trading at $130.00 though, you would have a loss of $9.00 or $900.00 real dollars. Your breakeven is at $121.00, since your 110/115 long spread offsets your extra short call’s risk from 115 to 120, and you collected $1.00 in extrinsic value premium up front, further enhancing your breakeven to $121.00

Therefore, if the stock is at $130.00, you would have a net difference between your breakeven of $121.00 and the stock price of $130.00, resulting in a $900.00 loss.

tastylive Approach

Our go to ratio-spread is a front-ratio spread. We normally do not route back-ratio spreads, which is where we are purchasing more options than we are selling, because this would be routed for a debit. We always prefer to collect premium and put ourselves in high probability situations. The beauty of this trade is that if we’re directionally wrong, it doesn’t matter if our spread expires OTM as long as we collect a credit - that will then be our profit. We route front-ratio spreads as a means to get into a long or short stock position with a very beneficial breakeven point. We tend to use these strategies if we have a price target in mind for the underlying. We will usually place our short strike at that target, as that would yield max profit at expiration if the stock ends up there.

Front Ratio Spread Profit and Loss

Ratio spreads have the potential to profit even if the underlying were to continue to decrease or increase slightly, because there is no risk to the OTM side when routed for a credit, and max profit is to the ITM side. We can remove risk because front ratios have more short options than long options, which allows us to enter the total trade for a net credit and contributes to extending our breakeven price further OTM past our embedded long spread. With a put front ratio, the risk is to the downside well below the embedded long put spread, and call front ratios have upside risk well past the embedded long call spread.

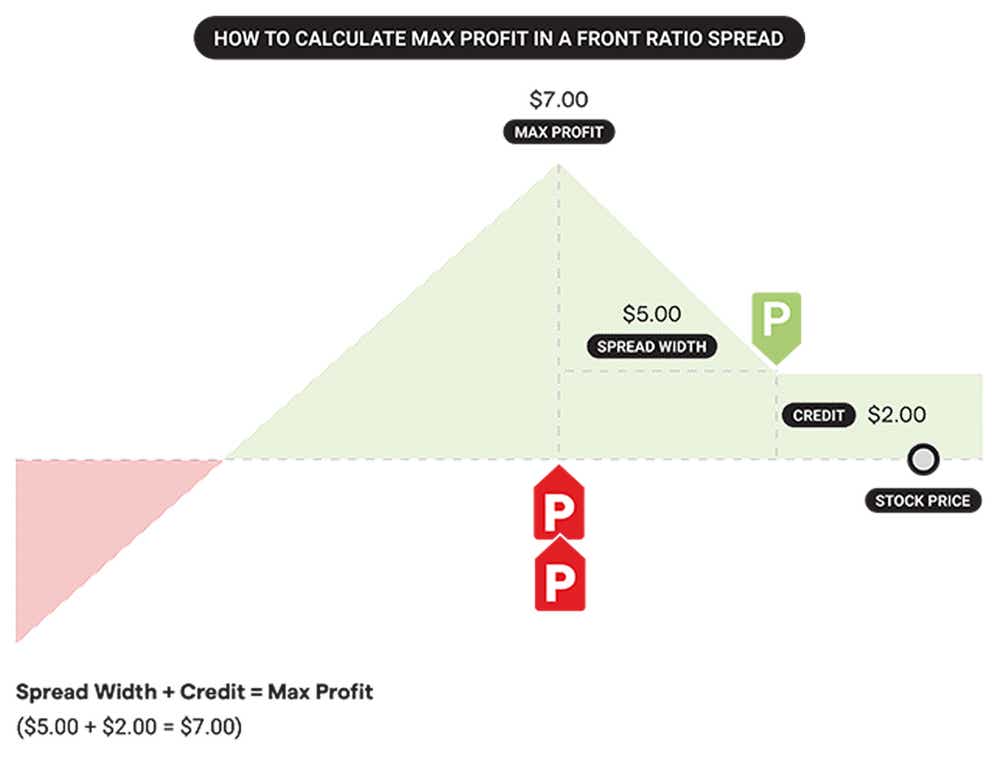

Front Ratio Spread Max Profit

On both call and put front ratios, max profit is achieved when the underlying’s price pins right at the short strike at expiration. Max profit occurs when the long vertical spread is fully ITM at the short strike, i.e. stock moves towards the short strike near expiration, and the short strike is ATM with little to no intrinsic value.

To calculate the maximum potential profit on a front ratio (as in the image below), simply determine the width of your vertical spread and add the credit received up front for entering the trade.

For instance, if you have a $5.00 wide vertical spread, and pick up an additional $2.00 in credit (because of the extra option you’re selling), your total maximum profit would be $7.00 (7 x 100 shares = $700.00).

If the stock continues in the direction where you’ve removed the risk instead, the options will continue to get further OTM.

Even though you can’t achieve maximum profit, you’ll still keep the credit you received when the strikes expire OTM (in other words, $200.00).

FRONT RATIO PUT SPREAD MAX PROFIT

Distance Between Long Strike & Short Strike + Credit Received

FRONT RATIO CALL SPREAD MAX PROFIT

Distance Between Long Strike & Short Strike + Credit Received

Front Ratio Spread Probability of Profit

However, a high POP does not necessarily translate to a high probability of achieving maximum profit. Remember, in order to achieve maximum profit, the underlying must pin at your short strikes at expiration.

FRONT RATIO PUT SPREAD BREAKEVEN

Short Put Strike - Max Profit Potential

FRONT RATIO CALL SPREAD BREAKEVEN

Short Call Strike + Max Profit Potential

Front Ratio Spread Risk

With front ratio spreads, there’s undefined risk if the underlying price moves past your breakeven point. For this, traders shouldn’t only consider their strikes to buy and sell, and maximum profit, but also the price in which they believe the underlying won’t breach before expiration.

How to Manage Front Ratio Spreads

Managing a Call Front Ratio Spread

The management concept is similar between a call front ratio spread and a put front ratio spread. However, with a call front ratio spread, the breakeven can be less favorable (you’ll have a narrower embedded long call spread) than in a put ratio spread if there is volatility skew to the put side – in other words, if equidistant OTM options from the stock price are trading for different values, specifically the OTM put trading for a higher amount than the OTM call. (see SPY options for a good example of put skew)

So, when you’re buying a call and selling two calls that are further OTM, they’re probably going to be trading for less than selling an OTM put option if you were to compare ratio spreads on both sides of the market. You’ll need a more narrow call ratio spread to still be routed for a credit compared to a put ratio spread. The key takeaway – there isn’t as much premium in further OTM calls in products that have put skew.

How you could manage a call front ratio spread without altering the trade:

Managing a Put Front Ratio Spread

When it comes to managing a put front ratio spread, you have more leeway than with the call ratio spread, due to breakeven being significantly improved in put skew environments, and with no risk to the upside. So, even if your extra short put is ITM, it’s likely not too far off your breakeven.

When it comes to managing your put, try to extend the duration and reduce cost basis. Also decrease your initial max loss consistently or hold on to it until you see a price reversion.

How you would manage a put front ratio spread without altering the trade:

Closing and Defense

WHEN TO CLOSE

When the position reaches 25% to 50% of maximum profit potential.

WHEN TO DEFEND

When the debit spread portion of the trade can be closed for near max profit, the debit spread portion can be sold while holding the additional short option. If the trader wants to extend duration on the position, the short option can be rolled to the next month.

What’s a Back Ratio Spread?

A back ratio spread is the inverse of a front ratio spread. In essence, you’re buying more options (put or call) than you’re selling. It’s more expensive, but the profit potential is unlimited with the extra long option. This trade is routed for a debit instead of a credit as well, so the max loss is to the OTM side, and equivalent to the debit paid up front for the trade.

A back ratio spread is structured as follows:

- Combination of one ATM short option (sell the call or put close to the current market price)

- Two ITM long options (higher puts or lower calls)

In a back ratio spread, or ZEBRA spread as we call it on tastylive, we focus on buying two ITM options and selling one ATM option for zero extrinsic value. This brings the breakeven price to the stock price, resulting in a 50/50 probability of success and close to 100 delta, without all the risk of owning 100 shares of stock.

A typical strategy that investors use with a back-ratio spread component is the ZEBRA stock replacement strategy. ZEBRA is short for zero extrinsic value back ratio spread and it isn’t a high probability trade. Instead, it’s a near-100 delta stock replacement strategy with all of the upside profit potential, with a fraction of the risk compared to owning 100 shares of stock (or being short 100 shares of stock with a put ZEBRA).

What’s a Call Back Ratio Spread?

A call back ratio spread is a neutral to bullish strategy, which benefits from a big bullish in the underlying. To create a call back ratio spread you’ll purchase two ITM calls and sell an ATM/OTM call against the long options to reduce the cost basis and ideally remove the extrinsic value from the trade.

A call back ratio spread typically consists of:

- 2x Long ITM call options

- 1x Short ATM/OTM call option to offset extrinsic value in the long options

The strategy is generally placed for a net debit so risk is to the OTM side or downside. The max profit is infinite, since we have an extra long call that has unlimited profit potential and there is no cap on how high an underlying’s price can go. With that said, we can calculate profit targets by taking the distance between the long ITM call and the stock price, less the debit paid up.

What’s a Put Back Ratio Spread?

A put back ratio spread is a bearish strategy that has no downside risk and benefits from a large selloff in the underlying’s price. This strategy is executed by purchasing a put debit spread with an additional long put at the long strike.

So, a put back ratio spread typically looks like this:

- Buy two ITM put options

- Sell one OTM/ATM put option at a lower strike price to offset the extrinsic value in the long options

A put back ratio spread has a short delta bias, which will profit from the underlying moving lower. Max loss is realized if the spread is OTM at expiration, and max loss is the debit paid up front.

The max profit is calculated by finding the distance between the long ITM strike and the stock price, less the debit paid. The breakeven is calculated by subtracting the debit paid from the long strike.

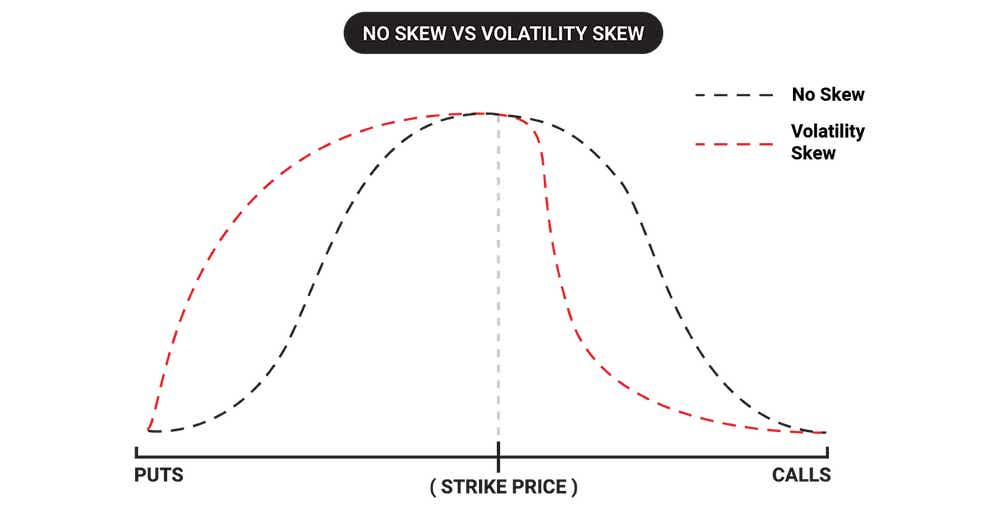

Impact of Volatility Skew on Ratio Spreads

A volatility skew, also known as an options skew, gives you a general idea of where the market perceives the risk of a big move to be. If equidistant OTM options when you compare puts and calls are trading at different values, there is skew in the market. The existence of put skew can be attributed to past crashes of the market.

In the graph below, you’ll see there’s put skew bias with the puts trading richer than the equidistant OTM calls. This happens because trades are hedging their long stock positions by purchasing puts, which increases their value and creates the skew.

What we can gather is that not all options on the same underlying and expiration have the same pricing when comparing equidistant OTM options on both sides of the market. In this example the puts hold their value the further OTM we go. For calls, the value decreases quickly because of this volatility skew on the put side. This doesn’t tell us where the market is going, it just tells us where the market participants perceive a potential high velocity move to be.

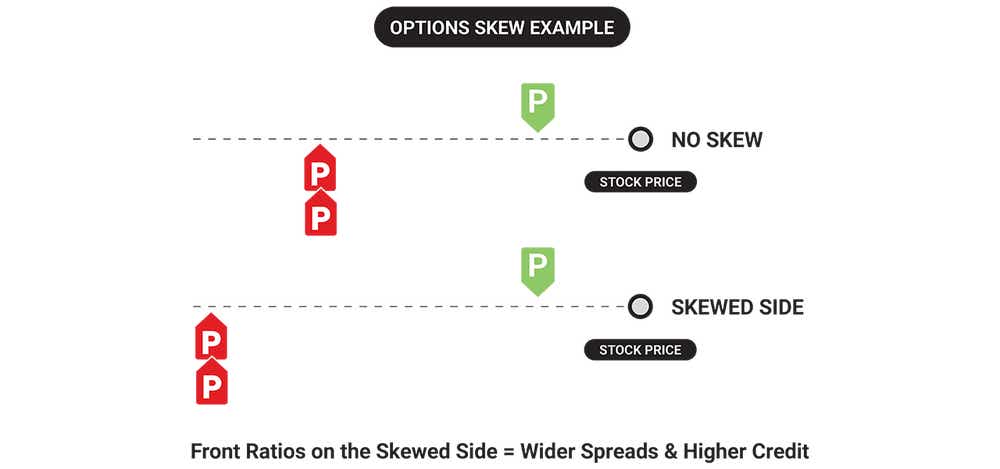

So, how does an options skew impact a ratio spread and why can this be an advantage for a trader?

Ratio spreads with the short option on the skewed side gives you the opportunity to have a very wide breakeven.

A ratio spread on a skewed side will allow you to collect more premium, for the same distance of width spread, compared to the non-skewed side. This means you can go further OTM for the same credit, or collect more credit for the same distance OTM.

Let’s say you take a put front ratio spread, where you’re buying a long option and selling two further OTM options against it to turn the trade into a net credit. If you place this front ratio spread on the skewed side of the market, we can make it much wider.

In the example below, the two short options are placed much further from the long option because of the put skew.

Ratio Spread Summed Up

- A ratio spread combines both long and short options of the same type with varying ratios of long and short options (i.e 2:1)

- Front ratio spreads have a high probability of success, as they allow you to collect premium up front and remove risk to the OTM side

- The max profit for the front ratio put or call spread is the distance between long strike and short strike, plus the credit received

- A back ratio spread consists of an ATM short option that’s used to finance two OTM long options, and is more of a stock-replacement strategy with limited risk.

FAQs

Is a ratio spread profitable?

Learn more about ratio spread profit and loss

What’s the difference between vertical spreads and ratio spreads?

The main difference between the two is that with a ratio spread the number of options that you sell aren’t equal to how many option contracts you buy and vice versa. A vertical spread is composed of equal amounts of long or short puts or calls at different strikes by expiring at the same time. Front-ratio spreads turn vertical spreads from debit trades into credit trades with no risk to the OTM side by adding an extra short option to finance the entire trade.

What’s a back spread in options?

A back spread in options is the inverse of a front-ratio spread. In this case you’ll buy twice as many put or call options than you sell.

How do you calculate spread ratio?

Spread ratio is calculated by determining the difference between the long and short options. For example, if I buy 2 options and sell 1 in a back-ratio spread, that is a 2:1 ratio spread.

If I sell 3 options and buy 2 options, that is a 3:2 front-ratio spread.

How do I manage ratio spreads?

To manage your ratio spread, you need to keep an eye on the position to close it on time to minimize risk and maximize profit potential. The debit spread portion of the trade can be closed for near max profit if the spread is ITM, while defending the additional short option. In order to extend the duration on the position, the remaining short option can be rolled to the next month.

What’s a call ratio spread?

A call front ratio spread is made up of a long call and twice as many further OTM short calls where the entire trade is a credit on trade entry. It has a short delta bias, which profits from the underlying moving lower equivalent to the credit received up front, but max profit is realized if the underlying moves slightly higher to the strikes of the short options.

A call back ratio spread is made up of two long calls that are ITM and one short call ATM/OTM to remove the extrinsic value of the trade. This creates a near-100 delta stock replacement strategy, but with much less risk than 100 shares of stock due to the defined risk nature of the trade.

SUPPLEMENTAL CONTENT

Episodes on Ratio Spreads

No episodes available at this time. Check back later!

tastylive content is created, produced, and provided solely by tastylive, Inc. (“tastylive”) and is for informational and educational purposes only. It is not, nor is it intended to be, trading or investment advice or a recommendation that any security, futures contract, digital asset, other product, transaction, or investment strategy is suitable for any person. Trading securities, futures products, and digital assets involve risk and may result in a loss greater than the original amount invested. tastylive, through its content, financial programming or otherwise, does not provide investment or financial advice or make investment recommendations. Investment information provided may not be appropriate for all investors and is provided without respect to individual investor financial sophistication, financial situation, investing time horizon or risk tolerance. tastylive is not in the business of transacting securities trades, nor does it direct client commodity accounts or give commodity trading advice tailored to any particular client’s situation or investment objectives. Supporting documentation for any claims (including claims made on behalf of options programs), comparisons, statistics, or other technical data, if applicable, will be supplied upon request. tastylive is not a licensed financial adviser, registered investment adviser, or a registered broker-dealer. Options, futures, and futures options are not suitable for all investors. Prior to trading securities, options, futures, or futures options, please read the applicable risk disclosures, including, but not limited to, the Characteristics and Risks of Standardized Options Disclosure and the Futures and Exchange-Traded Options Risk Disclosure found on tastytrade.com/disclosures.

tastytrade, Inc. ("tastytrade”) is a registered broker-dealer and member of FINRA, NFA, and SIPC. tastytrade was previously known as tastyworks, Inc. (“tastyworks”). tastytrade offers self-directed brokerage accounts to its customers. tastytrade does not give financial or trading advice, nor does it make investment recommendations. You alone are responsible for making your investment and trading decisions and for evaluating the merits and risks associated with the use of tastytrade’s systems, services or products. tastytrade is a wholly-owned subsidiary of tastylive, Inc.

tastytrade has entered into a Marketing Agreement with tastylive (“Marketing Agent”) whereby tastytrade pays compensation to Marketing Agent to recommend tastytrade’s brokerage services. The existence of this Marketing Agreement should not be deemed as an endorsement or recommendation of Marketing Agent by tastytrade. tastytrade and Marketing Agent are separate entities with their own products and services. tastylive is the parent company of tastytrade.

tastyfx, LLC (“tastyfx”) is a Commodity Futures Trading Commission (“CFTC”) registered Retail Foreign Exchange Dealer (RFED) and Introducing Broker (IB) and Forex Dealer Member (FDM) of the National Futures Association (“NFA”) (NFA ID 0509630). Leveraged trading in foreign currency or off-exchange products on margin carries significant risk and may not be suitable for all investors. We advise you to carefully consider whether trading is appropriate for you based on your personal circumstances as you may lose more than you invest.

tastycrypto is provided solely by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. Neither tastylive nor any of its affiliates are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors due to the number of risks involved. The value of any cryptocurrency, including digital assets pegged to fiat currency, commodities, or any other asset, may go to zero.

© copyright 2013 - 2026 tastylive, Inc. All Rights Reserved. Applicable portions of the Terms of Use on tastylive.com apply. Reproduction, adaptation, distribution, public display, exhibition for profit, or storage in any electronic storage media in whole or in part is prohibited under penalty of law, provided that you may download tastylive’s podcasts as necessary to view for personal use. tastylive was previously known as tastytrade, Inc. tastylive is a trademark/servicemark owned by tastylive, Inc.

Your privacy choices